While we normally find ourselves captivated by high-frequency economic data releases such as monthly retail sales and mobile device traffic, it is equally beneficial to examine the complexion of the consumer bedrock on which we rest. It’s no secret that, for many reasons, the period between 2008 and 2020 was one of the most challenging for retailers. In particular, the retail sector faced two major structural headwinds: demographics and homebuilding.

Where Have All The Big Spenders Gone?

It is difficult to recognize paradigm shifts in real-time. Sometimes these changes happen rapidly, but most of the time they happen in slow motion. Changes in the demographic composition of a population are of the slow-moving variety; however, they’re one of the easiest paradigm shift triggers to spot. For instance, much attention has been given to the aging Baby Boomer population, and developers have rushed to meet the expected increase in demand for senior housing.

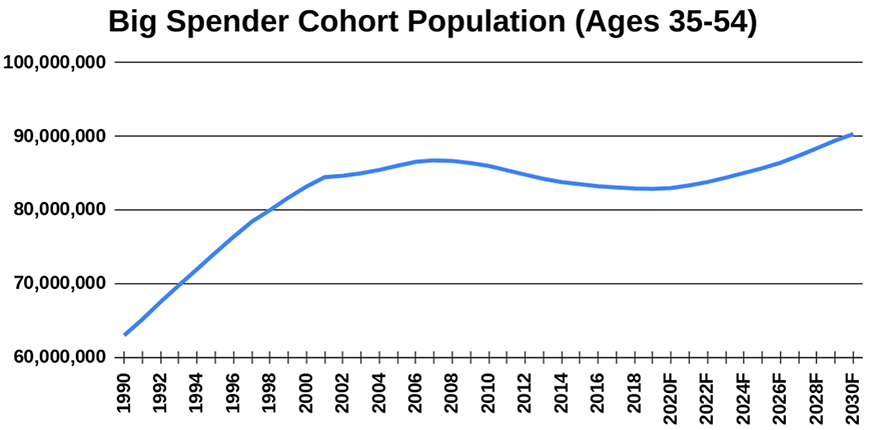

High Level of Spending Associated with Housing and Children

Of course, other demographic shifts have largely flown under the radar. And, since demographics are our destiny, it is worth exploring changes within the “Big Spender” cohort, which is defined as people between the ages of 35-54. Why is this segment of the population called Big Spender? If you can’t guess, then you’re probably younger than 35. In short, it’s because of the high level of spending associated with housing and children: clothes, larger homes, furniture, vacations, camps, food, electronics, larger cars, entertainment, school-daycare-aftercare expenses…the list goes on. Naturally, one must also have access to more money in order to spend more money, so it is worth noting these are the peak earning years for most people as well. Moreover, regardless of one’s familial situation, there is a proclivity to spend more if one is earning more. Bottom line, retailers thrive when the population of Big Spenders is growing…and spending.

Source: OECD.Stat; Davenport Consulting

As you can see in the above chart, the Big Spender population contracted during each and every year beginning in 2008 through 2019; 12 dismal years culminating in a 4.5 percent decline. For some perspective, since 1960 a contraction in the Big Spender population has only occurred during two other years: 1969 (-0.13%) and 1975 (-0.1%). So, to say the U.S. has just exited the strongest demographic headwind its retailers have faced post-WWII would be an understatement. Moving forward, growth in the Big Spender cohort will once again resume, albeit at a moderate pace, and the growth will continue through at least 2030. Relatively speaking, retailers are poised to enjoy the strongest demographic tailwind they’ve seen since before the Great Financial Crisis.

Houses Are Full Of Stuff…

According to the Census Bureau, in 2019 the average size of a newly constructed house was 2,301 SF, while the average size of a newly constructed multifamily unit (intended for rent) was 1,057 SF. How does a new homeowner fill a space that is ~1,250 SF larger than their former rental unit? Answer: they buy A LOT more stuff! But, homebuilding isn’t what it once was…

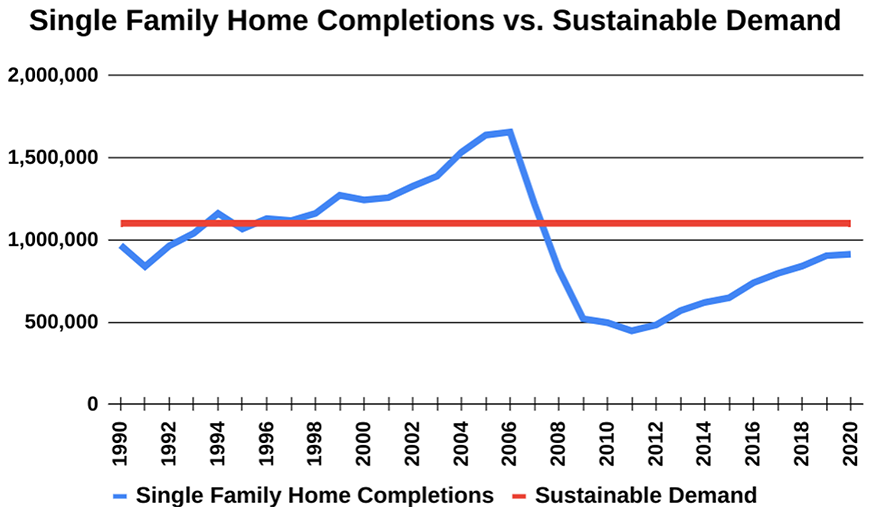

Source: Census Bureau; HUD; Davenport Consulting

Depending on whom one asks, there is currently and has previously been, a need for somewhere between 1.1 million and 1.3 million new single-family homes, annually. This chart (red line) reflects the more conservative figure of 1.1 million. While the housing boom-bust is evident in the chart, what isn’t as apparent is the net deficit of single-family home completions contrasted with the demographically generated demand which has accumulated since 2000. Using the conservative figure of 1.1 million new homes needed, the deficit would be 3 million, while the more aggressive need of 1.3 million would put the deficit near 7 million new homes. Either way, we need home builders to significantly pick up the pace of building single-family homes – far above the 2019 and 2020 rate of 900,000 homes, annually. Eventually, they will. And, when they do, retail will see the headwind of depressed home building turn into a tailwind of accelerating home building. When that happens, more people will need more stuff, and retailers will be waiting with open arms.

Growing Into Our Retail Shoes

Classic advice never goes out of style. And, after the total stock of shopping center space increased by a dizzying 73 percent between 2001 and 2011, retailers and shopping center developers alike had no choice but to put down the shovel.

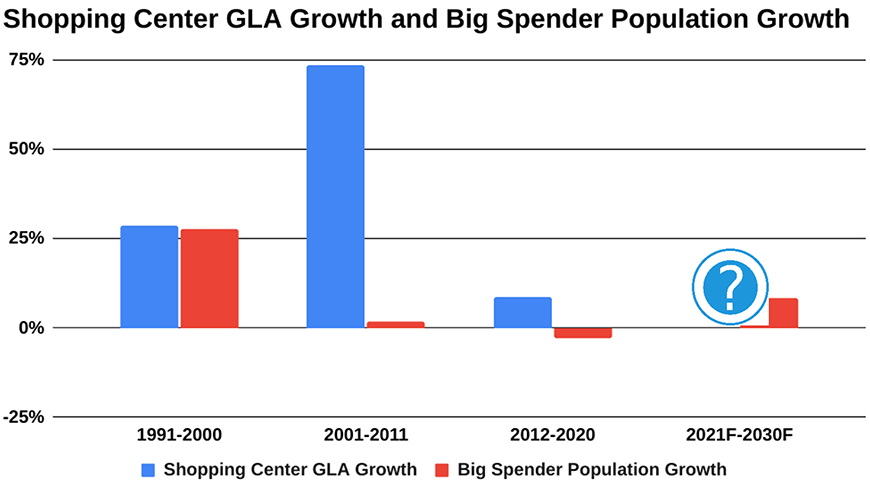

Source: Directory of Major Malls / ShoppingCenters.com; Davenport Consulting

Using data from Directory of Major Malls / ShoppingCenters.com, we can see that the rational retail development pipeline in 1991-2000 gave way to, well, let’s just call it ‘excessive exuberance’ during the 2001-2011 period, followed by a shopping center development depression ever since. But, the silver lining is that, once we stopped digging (both literally and figuratively), the healing began as the cannibalization ebbed. In fact, by 2015 the competitive shopping center vacancy rate, which carves out high-vacancy shopping centers, had already tightened back down to pre-recession levels. Point being, in less than a handful of years the retail market had already decided which shopping centers were viable and which were not, thus, reconciling much of the oversupply situation. A very Darwinian outcome, indeed.

Then came the pandemic. While the situation remains somewhat opaque, we know a few things for certain. First, shopping center vacancy has increased even in the best shopping centers. Second, the healing has already begun as retail sales have surged over the past year, and there is an estimated $2.2 trillion in excess consumer saving due to the lockdowns and government stimulus payments. And, lastly, the retail development pipeline has been relatively dry for years, which removes the ‘piling on’ threat of new deliveries and cannibalization.

Conclusion

While we’ve previously proven the “Retail Apocalypse” was an exercise in gaslighting, that’s not to say the past 10-15 years have been particularly kind to retailers. Demographic erosion, depressed levels of homebuilding, and a particularly tough bout of shopping center oversupply conspired to make this, arguably, the most difficult period retailers have faced post-WWII. However, this too shall pass as these headwinds are poised to reverse direction, becoming tailwinds. Moreover, consumer balance sheets are in excellent shape, and their ability to spend is profound as evidenced by current trends in retail sales. For retail sector participants, the building blocks for the next 10 years look far more constructive than those of the prior 10 years. The winds of change have arrived, and they favor retail.

About Jeff Davenport

Jeff Davenport is a data geek who talks in his sleep about commercial real estate. To pay the bills he takes a dash of economic data, a pinch of demographic data, a teaspoon of CRE data, and a splash of common sense to create a large helping of actionable intelligence. He has spent the past two decades in commercial real estate development, leasing/sales, research, and advisory roles. You can connect with him on LinkedIn: https://www.linkedin.com/in/jdavenport5/