Given the tremendous amount of uncertainty and change thrust upon the economy this last year during the pandemic, The Directory of Major Malls, Inc. is proving that continuity and agility are still the best ways to make what’s old, new again.

Given the tremendous amount of uncertainty and change thrust upon the economy this last year during the pandemic, The Directory of Major Malls, Inc. is proving that continuity and agility are still the best ways to make what’s old, new again.

Having been a player across the retail landscapes of the US and Canada for almost 40 years, Directory of Major Malls (DMM) has continued to be a leading source of shopping center and mall information and has therefore expanded the uses and relevance of the collection and maintenance for data over many years of major shopping center and mall data. It makes no difference if your primary focus is in Investments, Development, Leasing, Retail Expansion, or even Support Services for a shopping center, DMM data provides an inroad to the contacts, retail stores, and people activity of centers that have Gross Leasable Areas (GLA) of approximate 200,000 square feet and up.

The declines in retail traffic brought on by Covid-19 is unlike anything seen in recent memory, but it has generated new enthusiasm for clean, accurate data that can help reshape how retail is bouncing back and plans to be a key driver in the future growth of the economy.

So the question is, Did the retail shopping at the physical location really disappear from large shopping centers, never to return?

The answer is emphatically NO! The pandemic created a shift, a new awakening, and a forced renaissance about how major shopping centers and malls are configured and engage with customers. The DMM dataset proves out this transformational resurgence that is shifting brick and mortar configurations and uses once again. Even though the pandemic brought about a significant increase in online shopping, that still did not come close to erasing the damage done when physical stores were closings and economic worries increased.

Much like the butterfly emerging from its cocoon after an extended slumber, shopping centers and malls are reemerging in equally brilliant fashion. Analysis of recent data managed and sold exclusively by DMM through direct licensing and on a subscription-based on ShoppingCenters.com, we can see that more than 20% of larger conventional enclosed malls have plans to convert to hybrid configurations which combine Retail, Office, Residential and other alternative uses in the next few years. The DMM data when analyzed in the current year or over time, pinpoints many types of shifts that create opportunities across the board. Knowing answers to question like:

- What is happening with the over 5,000 anchor space vacancies associated with more than 1,500 of the major shopping centers and malls tracked in DMM?

- What is the current tenant mix for each center and how has it changed over time?

- Which Owner Developers are the largest & smallest contributors to the major shopping center dataset?

- Gross Leasable Area?

- Stores & Store Categories?

- What is the overall traffic in a center?

- What are the demographic components with a specified radius?

All of these questions and many more are being answered by accessing the breadth and depth of data owned by DMM and can be used to garner the growth that is planned as we emerge from the pandemic. In a recent study, The National Retail Federation, the world’s largest retail trade association, who passionately advocates for the people, brands, policies, and ideas that help retail thrive, forecasted that 2021 retail sales are estimated to total between $4.33 trillion and $4.4 trillion. That’s a significant uptick that will most definitely include sales from existing and new shopping centers and malls.

DMM is continuing its prominence as a premier source of shopping center and mall data and its desire to keep pace with this economic revitalization, by initiating strategic partnerships, both business & data, to enhance the experience and usefulness of the DMM dataset. One such partnership is with B I Spatial of Greensboro, NC. B I Spatial operates as a premier Geospatial, Business Intelligence service, and technology provider with extensive experience in serving multiple industry segments, such as Retail Chains, Private & Publicly Traded Retailers, Grocery Chains, Hedge Funds, and REITs as well as landowners or developers as it pertains to segmentation and site selection analytics.

B I Spatial is currently providing DMM with additional data components through the use of technology, segmentation, and mobile location data from Near (formerly UberMedia). These analytic attributes enhance the insights, use cases, and value of the DMM dataset to its subscribers and licensees.

Our alliance with B I Spatial led to the creation of a proprietary set of Shopping Center Geofences and Retail Boundaries that allow for traffic/people data over time to be joined with the base data of each center. The traffic data is further enhanced by appending segmentation data which now rounds out who the true customers of the center are and what are the psychographics that drives their retail behaviors.

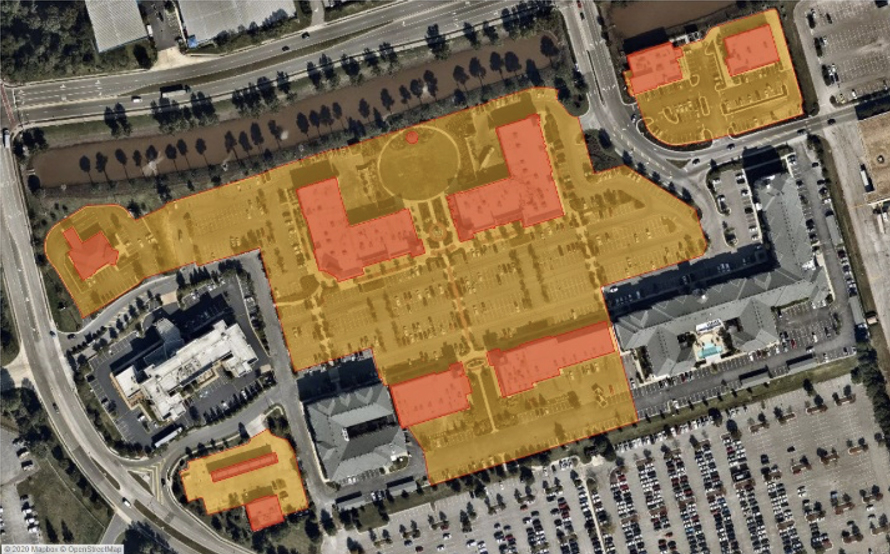

DMM Shopping Center Geofences are virtual spatial boundaries specific to a DMM shopping center or mall. The Shopping Center Geofence corresponds to the published layout of the center or mall taking shadow anchors and the parking into consideration.

DMM Retail Boundaries give specific attention to the retail environment around and including the DMM shopping center or mall. Not every adjacent structure contributes to the retail environment. Any derived insight using the DMM Retail Boundary will be solely retail-centric and relevant.

Overlaying traffic data combined with new configurations and the psychographics attached to that human activity turns the DMM dataset into a sophisticated tool that drives business decisions about a particular center and/or the market area surrounding it. One major example of how the complete dataset with traffic data becomes a driver to growth after the pandemic is that one can start to understand the migration patterns of old and new customers. The pandemic created a massive migration of people from one location to another, some temporary and some permanent. In either event, the retail profiles of activity shifted along with the people. Knowing WHAT changed is made more relevant when you identify WHO made up the change.

Through our strategic alliance with B I Spatial’s Precision with Privacy™ (PwP™) product, a monthly, spatially anonymized dataset containing the most representative residential points of mobile devices in the United States which can be coupled with various available commercial segmentation schemas. The PwP™ dataset provides deeper insights into the specific migration patterns or shifts that can be seen in the more than 73 Million devices represented in the sample set. These people movements have a tremendous impact on the new retail efficacies of a shopping center or mall. The data provides a few examples of how impactful the traffic data can be when the details are associated to the DMM dataset through licensing and custom analytics.

Of the most current 73.7 million device records in the PwP™ database from March 2020, we followed those devices for the remaining 9 months of 2020. Some of the National statistics show:

By Segmentation

The biggest shift was among the youngest segments who are just getting started in their adult lives, including college students who moved back at home in March of 2020.

By Geography

- 1% moved to another Census Block Group

- 1% moved to another county

- 6% moved to another state

By Distance

- 4% moved at least 3 miles

- 6% moved at least 5 miles

- 3% moved at least 10 miles

- 7% moved at least 100 miles

- 5% moved at least 500 miles

When you start to look at migration patterns across some select markets there are some consistent patterns across each.

- In every market, the central-most and most heavily populated county led its market in decreases, both in raw numbers and percentages. Typically, the movers went to surrounding, less dense counties.

- Chicago (Cook County)

- 39% of those moving out stayed in IL

- 35% of those moving out stayed in the neighboring IL counties

- IN, FL, WI, and MI led the out-of-state destinations

- Seattle (Kings County)

- 53% stayed in WA

- 33% moved to nearby Pierce and Snohomish counties

- CA was the #1 destination of King County movers

- OR, TX and AZ led the out-of-state destinations

- Nashville (Davidson County)

- Only 4% of movers left the 14-county metro

- 68% of Davidson County (Nashville) movers stayed in the metro

- 50% + stayed in TN

- FL, GA, and TX led out-of-state destinations

- Denver (Denver County)

- 4% of devices left the 10-county metro

- 58% of Denver County movers stayed in the metro

- 69% of Denver County movers stayed in CO

- TX, FL, and CA led out-of-state destinations

- Chicago (Cook County)

It’s apparent that the migration patterns in markets throughout the US will continue to shift as will the shopping center properties as they transform to better serve the new demands of the consumers. New patterns will emerge which are more synergistic with consumer behavior and the integration of omni-channel purchasing.

About Directory of Major Malls, Inc.

What started in print in the late 1970s as the Directory of Major Malls, decades later has evolved decades into THE industry source for comprehensive and accurate major shopping center and mall retail data. The Directory of Major Malls’ inventory of centers focused on the over 17,600 major US and Canadian shopping centers and malls, the 367,862 associated tenants within those properties and nearly 52,624 primary retail real estate contacts provide a vast wealth of retail intelligence. Just as the markets we serve, The DMM Data is continuously updated & evolving. Our proprietary technological research methods are combined with direct data collection from Owners, Landlords and other Human vetting processes make the DMM dataset one of the longest and most sought-after datasets to date. Accessed via multiple methods including online, direct licensing, consulting services, and reselling channels, the DMM data is poised to allow a deep-dive strategic analysis of historical retail trends and support forward-thinking advances for retail shopping center leasing, development, and investment.